Understanding and Negotiating Rent to Own Contracts

Rent to own agreements are unilateral contracts, meaning only the seller is bound by it to take action at the end of the lease. That means the seller must sell the house should the buyer choose to buy. However, the buyer is not contractually obligated to buy the home.

That’s why there are so many incentives worked into the contract to convince the buyer not to buy, like losing rent credits and the option fee.

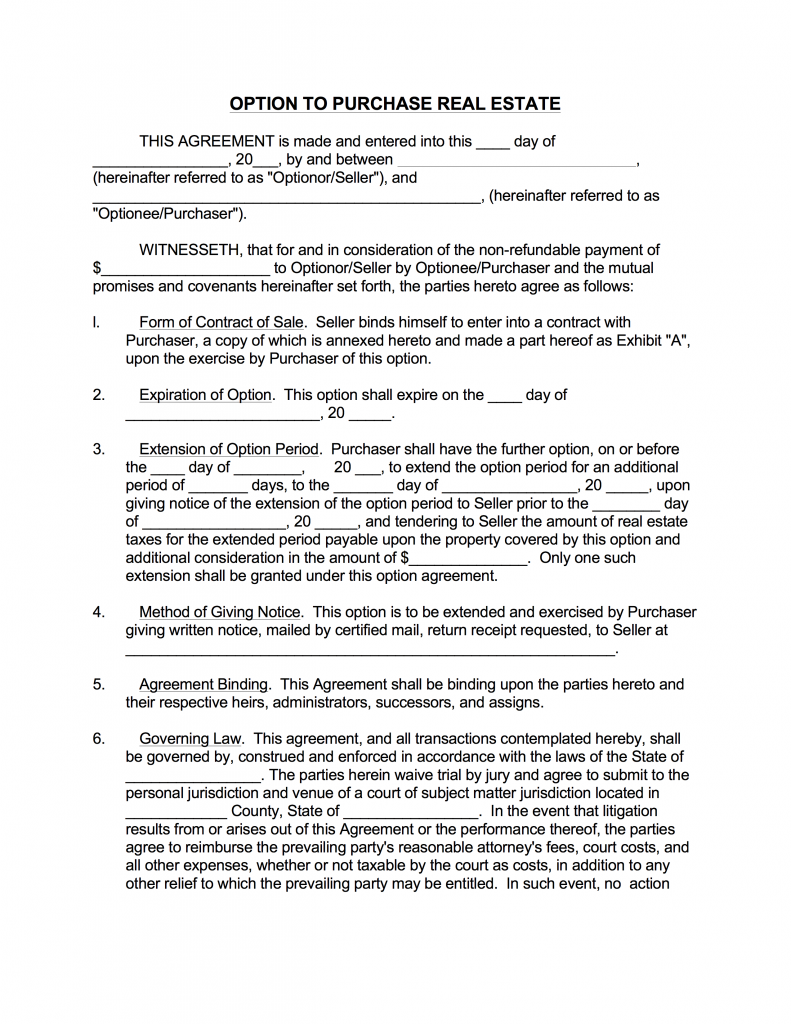

Your typical option to purchase contract will look like the one below. Click the image to download the PDF file.

Can You Negotiate a Rent to Own Contract?

There is a lot to negotiate in terms of rent to own – price, option fee, rent credits, rent premiums, the closing timeframe, repairs and more. Basically, anything in your contract is negotiable.

You can absolutely negotiate rent to own before you sign the contract. After the contract has been signed, there is very little that you can negotiate.

Purchase Price

There are two methods to setting the purchase price: fixed and at time of closing.

It's important to realize that you will probably get a win when it comes to purchasing price and a loss in the lease terms or vice versa. It is very rare that you get your way with both.

While purchase price is very important when you're buying a home outright, it is less important when you are renting to own.

Reason being, as a buyer, the purchase price is something you might pay. Meaning, not every person who rents to own buys the home. However, every person who rents to own leases. No matter what, you will pay an option fee, you will have a set timeframe that you must close within and you might have premium payments to make each month.

Those factors impact you more immediately and certainly than purchase price because you could choose to walk away from the home.

As a seller, the lease terms are important for the same reason. The seller will automatically keep the nonrefundable option fee and any rent premiums. However, there is no guarantee your home will be purchased.

Additionally, there is no way to figure out how the market will change. What might be a good deal now could be a terrible deal at the end of the lease.

Therefore, while purchase price is important it shouldn't be your negotiation focus when writing the contract.

In fact, you might want to delay setting the purchase price until when you close. That way both parties feel they are getting fair market value and no one can suffer tremendous loss.

You may want to state in the contract that the home will be priced at fair market value at the time of the home purchase, as determined by an independent appraisal, especially if you are the buyer.

At the time of purchase, the seller will have quite a bit of leverage on you (your money from the option fee and your rent credits). That means you won't be able to walk away from the deal – a key factor of negotiation. For that reason, you want to protect yourself in advance.

Closing Timeframe

When it comes to timeframe, the seller wants to get the property off his or her hands as quickly as possible. His or her only benefit from dragging it out is the added income that comes with monthly rent.

As a buyer, you want the longest timeframe possible because you can close early.

You want the timeframe to be long because you will have more time to qualify for a mortgage. If the lease is too short for you to qualify for the mortgage you'll lose all of the money you've saved up through your option fee and premium payments.

So, how does a buyer negotiate with the seller to get the longest timeframe possible for the closing date?

The first thing to know is that the shortest possible lease term is 12 months. While they can be as long as you and the seller agree to, the maximum is typically 36 months.

The best thing to do is be up front about how long you want the lease to be from the beginning. That way you and the seller will not waste time working on a deal that will not work.

To convince the seller of a longer lease term – should he or she be reluctant:

- Let him or her know that you only want a long timeframe to ensure that this deal will be successful. Remind the seller that if this deal isn't successful, he or she would lose even more time trying to find someone else.

- Remind the seller that he or she will be earning an income off of you throughout the lease term.

- Assure the seller that you plan to purchase the home; thus, letting the seller know that the wait will be worthwhile.

Option Fee

No matter how you negotiate it, the option fee is nonrefundable. The buyer is paying for the option.

The option fee is normally 2-5 percent of what the home is worth; although, it can go as high as 10 percent and can even be paid with something other than cash.

In some cases, you can use material possessions to pay your option fee (i.e. a boat, car, etc.).

In other case, buyers can exchange services for the option fee. For example, if the buyer works as a handyman, he or she could remodel the bathroom in exchange for a $5,000 option fee. It just needs to be inside the contract that the buyer will make that repair by a specified date.

The option fee helps the seller feel confident that you will purchase the home. The larger the option fee, the harder it will be for the buyer to walk away from the money.

In order to negotiate a better option fee, the buyer needs to make sure the seller feels confident that he or she will purchase the home without the money held as an incentive.

How can you make the seller feel more confident? Be confident.

Explain your plan to the seller. Tell him or her why you:

- Will be financially capable of paying for the deposit on the home when it is time to close.

- Will have a high enough credit score to qualify for a mortgage when it is time to close.

- Want to live in this beautiful home for the long term.

- Will take care of this home while you are staying in it as if it were your own – because you plan for it to be.

The last part is particularly important. Let's say you end up not purchasing the home. You move out and the seller is stuck having to find another buyer or find a tenant. Both of those are difficult if you didn't take care of the home while you lived in it. In fact, the seller will have to use the money from your option fee to repair the damage you left behind.

In that case, the seller would wish for a higher option fee to cover the damages and the time lost renting to you.

You need to reassure the seller that is not the case so that he or she is confident enough to lower your option fee. However, reassure them by stating how well you will care for the property, not by telling them about the above possibility, which could make them want to overlook your reassurance.

Rent Credits

A rent credit means that a percentage of the monthly rent goes into an escrow account. You can then use the money in that escrow account to pay the down payment on the home.

You don't necessarily need to have rent credits as part of your contract. Not everyone does. Rent credits simply incentivize the buyer to buy. They're definitely helpful for the seller's confidence and, in certain situations, they're helpful to the buyer too.

There are a few ways that a rent credit can work. I'll explain each assuming the fair market rent of the home is $1,000.

- Percentage of Fair Market Rent

- Matching

- Rent Premiums

So, the fair market rent for the home is $1,000. You and the seller set a percentage of that amount that you can use for your down payment on the home if you purchase it.

Let's say that the percentage is 10 percent. In this example, 10 percent of $1,000 is $100. So, in a 36-month lease, you will have saved $3,600 toward your down payment without really taking anything out of pocket.

This – by far – is the best method because you save money without losing any.

You can negotiate this option with the seller by letting him or her know this money will give you an incentive to purchase the home. The seller should know the money will make you more likely to purchase and they don't spend any of their own money giving you that incentive.

However, this also means the seller loses $3,600 of profit throughout the lease. If the seller does not want to let go of that profit, you have other options to still work with rent credits.

If you see the value of having money built up at the end of the lease to help with the down payment, you could try matching.

Going with the same example, fair market rent is $1,000. You tell the seller that you are willing to pay $1,100 a month. Sounds like a great deal for the seller, right?

Tell the seller you would be willing to pay 10 percent more if he or she is willing to match the money in an escrow account. That means that your $100 goes into the escrow account and the seller puts an additional $100 in the account to match it. Make sure the seller knows this money comes out of the rent you pay, not his or her pocket.

At the end of the 36-month lease, you will have $7,200 in a bank account. Should you choose to purchase the home, that $7,200 goes toward your down payment.

This is a pretty good deal for you and the seller, but only if you're sure you want to purchase the home at the end. Otherwise, the seller will keep the $3,600 you contributed out of pocket.

Remember that if you purchase the home, you'll get the money right back. However, that's only if you do purchase the home.

The last option isn't necessarily helpful to the buyer. The buyer pays extra money on top of fair market rent to the seller. The surplus money is kept in an escrow account, and the seller contributes nothing.

So, to continue with the example. Fair market rent is $1,000. The buyer pays $1,100 a month and has $3,600 at the end of the lease to use toward the down payment.

If the buyer doesn't purchase the home, the seller keeps this money.

Obviously, there is a benefit here for the seller; however, the buyer's benefit is not apparent without further analysis.

Remember some of the other items we've negotiated: timeframe and option fee. For both items, it was important to assure the seller that you are committed to purchasing the home.

Committing to paying an extra $100 a month demonstrates a commitment to purchasing the home. If you're attempting to negotiate timeframe and option fee, a buyer can use rent premiums as a bargaining chip.

Again, you only want to do this if you are sure that you will buy the home because if you do not buy you lose the money.

However, if you are certain that you will buy, it is not a bad option because you will get the money back to help purchase the home at the end of the lease.

Property Repairs

Whose job it is to repair damage to a rent to own property is not clear cut.

When you’re renting a home from a landlord, the landlord pays for repairs. When you own a home, you pay for repairs.

What if you’re in between?

That’s the case for anyone renting to own a property. It’s important to lay down the terms of whose responsibility each type of repair is in your contract, so there’s no arguing about it down the line.

Before you sign the contract, you should have the house inspected. Try to get the seller to pay for any major repairs that need to be made on the home before you move in, like the roof or A/C. If the seller will not make the repair, negotiate the cost of the repair off the final price of the home.

For example, if the home will be priced at $120,000 and the roof will cost $10,000 to fix, negotiate that the seller use some of the money you pay to fix the roof.

In terms of repairs that come up after you purchase the home, you can be liable for as little as repairs that cost $25 or less and as large as repairs that cost $200 or less, it all depends on how you negotiate the situation. If the seller wants to make you liable for anything more than $200, you can do it, but know that it is very uncommon.

Rent to Own Contract FAQs

Renting to own can be highly effective if done correctly. We can’t emphasize enough how important it is to ask these questions about your rent to own contract before signing the contract.

Before entering into a rent to own contract, there are a variety of details you should be careful with. By asking the right questions, you can minimize your chances of trouble or confusion during your lease. Here are some rent to own contract FAQs you should be asking:

- Who pays for maintenance, property taxes, and homeowner’s insurance?

- What is my monthly base rent and rent premium going towards?

- Is the purchase price determined in the rent to own contract?

- What fraction of the rent premium and option fee will the seller credit toward the home purchase?

- Under what conditions could the contract become void?

- Will the seller finance or will you need a mortgage?

Ordinarily, your landlord/seller will pay the property tax fees and homeowner’s insurance. This is because since he or she is still the legal homeowner and is ultimately responsible for the property. For a renter/tenant in a rent to own contract, this is an advantage for you. Without these liabilities, you will have more time to equip yourself financially.

On the other hand, renters are typically responsible for home maintenance fees and general housekeeping. In contrast to a traditional lease, a rent to own contract expects tenants to make their own repairs. This is because the tenant plans to own the home in a few years. In some cases, the landlord will pay for major repair costs if it exceeds a certain cost.

Essentially, it is crucial to understand who is responsible for paying the various types of costs. Your rent to own contract should clearly state how much time you have to fix a repair. It should also tell you what kinds of modifications you may make to the home. You and the landlord may negotiate the terms of the contract. However, don’t hesitate to consult a real estate attorney if you are unsure if the terms lie in your best interests.

Many renters are thrown off when they discover that rent to own payments are higher than normal rent payments. Usually, the seller will charge a high enough monthly base rent that will go towards the cost of their mortgage payment, taxes, and insurance fees on the home. Your monthly base rent is equivalent to the fair market rent, which is different from your rent premium. Your rent premium is simply the extra amount you pay per month in addition to your base rent, which the seller will credit back to you if you decide to purchase the home at the end of the lease.

Less commonly, the seller does not collect enough base rent per month to completely cover the cost of their mortgage payments and homeowner fees. This tends to happen when houses are on the more pricey end of the market, so the landlord must pay relatively high interest rates and high mortgage payments. In these cases, the landlord will have to pay the difference in the amount not covered by your monthly base rent.

Be aware that some landlords will attempt to evade the difference in the amount by charging higher than the market rate for monthly rent. Because of this, you should always check if your listed rent aligns with the fair market rent, which you can find out by contacting a mortgage lender or using the online tool Rentometer. If it does not, either negotiate a different price or go find a better deal!

In most rent to own contracts, the purchase price is an estimate of the home’s fair market value at lease-end and is agreed upon in the contract. Similar to the rent price, you and the seller determine the purchase price before the lease begins. It remains the same, regardless of whether the fair market value fluctuates or not. The purchase price does not lean in favor of either the seller or the tenant since nobody knows for sure what the future fair market value will be.

At the end of the lease, if the actual fair market value exceeds the estimated fair market value, the buyer will benefit since they will be paying less for the house than they normally would. On the contrary, if the actual fair market value falls below the estimated fair market value, the seller will benefit since they will be receiving more for the home than they otherwise would.

You may check the current fair market value of a home by using a home value estimator. However, if you need help evaluating what the future fair market value of a home will be, you are better off consulting a local mortgage banker.

For most rent to own contracts, the seller credits the total cost of your lease option fee and rent premium payments towards your down payment if you decide to exercise your option to purchase the home. A lease option fee, which you pay before the rent term begins, is a fee (usually 2-7 percent of the cost of the home) that guarantees you the option to buy the home in the future.

It is important to note that the lease option fee is NOT optional and every rent to own contract requires one. The lease option simply gives you the power, but not the obligation, to buy the home at any time during the rental period.

Generally, your option fee and rent premium payments are non-refundable; so if you decide to not purchase the home, you will probably not get this money back. In addition, many landlords are strict about timeliness. Some may even void your monthly rent credit if you do not make your rent payments on time. These conditions are characteristic of most rent to own contracts, but since every landlord is different, some may interpret the option fee or rent credit on their own terms. Because of this, you should always do your research, utilize your resources, and ask the landlord these important questions before entering into a transaction.

The landlord in a rent to own contract has the right to void the tenant’s contract if he or she violates lease responsibilities. Tenants can violate their lease in many ways. For example: keeping animals in the home if the lease is not pet-friendly, housing unwarranted people, participating in crime, and anything else specifically prohibited in the contract. Tenants may also be at risk of violating their lease if they make late rent payments or do not make necessary repairs, depending on the contract.

Often times, the contract may become void if the tenant is unable to qualify for a mortgage at the end of the lease. Unfortunately, many unethical sellers will purposely make it difficult for the tenant to secure a mortgage at the end of the term. There are 5 Ways to Spot a Rent to Own Scam that you should be aware of. These tips will help you to investigate the seller’s history and past transactions to make sure they are credible.

In some cases, the tenant may void the contract his or herself if the seller does not have marketable title to the property. When this happens, the landlord must reimburse the tenant for the costs of the title search as well as any of their rent payments made so far and the option fee.

Despite the many risks associated with a rent to own contract becoming void, remember that this may only happen if the tenant fails to meet his or her obligations. Everything the landlord expects of you should be clearly stated in the contract. Thus, it is imperative to review your contract’s terms before signing anything. If your contract has tricky wording, a real estate attorney can help clarify any questions you may have. As long as you consistently meet the expectations of your lease, your landlord will likely not have the means to void your contract.

Normally, the seller will not serve as a mortgage lender. Seller lending is more common in “contract for deed” sales rather than lease options. Instead, the buyer will have to find their own financing for a mortgage. Time frames vary between sellers, but generally, you must get a mortgage no later than one month after the buyer has made their decision.

You should seek advice from a mortgage broker prior to even entering a lease option. He or she will be able to gauge whether or not you will be able to qualify for a loan within the lease period. Although their predictions may not be 100 percent accurate, they can still provide you with valuable guidance.

Understanding Your Lease to Own Contract

Your lease to own contract is simple to understand if you know the parts it comes in and what to look into about it. Negotiate a contract that is beneficial to you. Read through your contract and understand what it means for each of the FAQs listed above.

Two Persons in Formal Attire Doing a Handshake by Raw Pixel is licensed under the Pexels Photo License.